The decision to determine local taxes and fees is a regulatory act. Therefore, decision-making regarding the determination of regional taxes and fees is subject to the Law "On the principles of state regulatory policies in the field of economic activity". That was the explanation of a lecturer from Podolia University from Ukraine who gave a Guest Lecture at STEKOM University.

How is the implementation of the existing taxation system in Ukraine in a state of war? Academics from state universities in Ukraine have given very clear and interesting explanations in an international seminar held by STEKOM University. The title of the Presentation was "Local tax: a system of calculation and payment under martial law in Ukraine". The name of the academic from the State University of Ukraine is Valentyna Borkovska. He has a PhD in Economics. Ms. Valentyna is an Associate Professor at the Institute of Education and Science in the department of Accounting, Business and Finance, at Podilia State University.

This activity is part of the implementation of STEKOM University's commitment to increase various international activities in order to realize the vision to become an international-class university. Various international activities carried out by STEKOM University continue from year to year. There are international activities that are sustainable and there are also some international activities that are not sustainable. All types of international activities are accommodated and regulated by the International Department of STEKOM University.

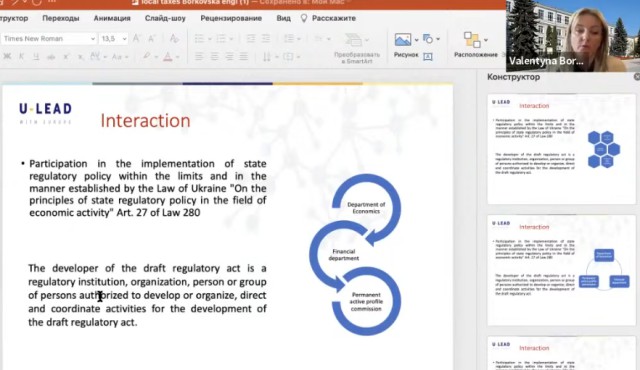

Ms. Valentyna then explained about the basics of tax law in Ukraine. He, certainty in the implementation of state regulatory policy within the limits and in the manner established by the Law of Ukraine "On the principles of state regulatory policy in the field of economic activity" Art. 27 Law 280.

The drafters of draft laws and regulations are institutions, organizations, people or groups of people who are authorized to compile or organize, direct, and coordinate activities for the development of draft laws and regulations.

Next, Ms. Valentyna explained the details about the land tax. In his explanation, the taxpayer is the owner of a plot of land or land that is divided into management and users. The tax base is adjusted to the normative monetary valuation index (valuation) of land parcels taking into account the coefficients. The area of the land parcels whose normative monetary assessment has not been carried out. The tax objects are land parcels owned or used and land parcels owned.

Ms. Valentyna also gave an explanation regarding the tax rates that apply there. Tax rates for land parcels, normative monetary assessments carried out (regardless of location):

- no more than 3% of the NMA plot

- for public land - not more than 1% of NMA

- for pretral and from 03% to 1% of your NMA

- for forests and not more than 0.2% of NMA

- for our permanent potting soil by business entities (except for state and communal forms after ownership) - not more than 12% of their NMA

For land parcels located outside settlements, the NMA has not been surveyed:

- for plots of land not more than 5% of NMA Land units on the outskirts of the area

- for aggregate - rom 0.3% t0 SX from NMA for rate line in the region

- for forest land» not more than 0% of NMA vn arable land in the region

As for the case of leased land, the explanation is as follows. The executive authority and local government must submit to the chartering agency the list against anyone and the convenience agreement has been made for the current year before 1 February. Land rents can exceed 12 percent in the case of land auctions. The basis for calculating the rent for a plot of land is the lease agreement for the 3 plots of land. The amount of annual rent is set in the range from the amount of land to 12 percent of the NMA. Changes in the annual rent amount depend on the approval of new NGOs in progress and on the value indexation coefficient of the normative monetary evaluation (valuation) of land, which is indexed by the NMA. The amount of rent must be uniform for one type of targeted land use (Law of Ukraine "On Protection of Economic Competition").

Visiting lecturer from Podilia State University of Ukraine 2022 teaching tax in wartime management Part 2

International Webinar

Kembali ke Berita

International Webinar

Minggu, 13 November 2022

Priyadi, S.Kom, M.Kom

0 Dilihat