A system of taxation of the income of a person imposing a tax on the income of individual taxpayers, regardless of their origin, at a uniform flat rate. This system was adopted by most of the countries of Central and Eastern Europe at the transitional stage.

How is the implementation of the existing taxation system in Ukraine in conditions? Academics from state universities in Ukraine have given very clear and interesting explanations in an international seminar held by STEKOM University. The title of the Presentation was "Local tax: a system of calculation and payment under martial law in Ukraine". The name of the academic from the State University of Ukraine is Valentyna Borkovska. He has a PhD in Economics. Ms. Valentyna as Associate Professor Educational and Scientific Institute in the department of Accounting, Business and finance, at Podilia State University.

This activity is part of the implementation of STEKOM University's commitment to increase various international activities in order to realize the vision to become an international-class university. Various international activities carried out by STEKOM University continue from year to year. There are sustainable international activities and there are also some unsustainable international activities. All types of international activities are accommodated and regulated by the International department of STEKOM University.

Next, Ms. Valentyna explained the basic principles of fixed tax administration. The establishment of fixed taxes in Ukraine is divided into 4 groups. Based on the taxpayers, the first group is private people or entrepreneurs. They do not use hired labor. The amount of income does not exceed UAH 1.0 million. The second group is entrepreneurs whose employees are not more than 10 people and whose income is not more than UAH 5 million. The third group is legally registered entrepreneurs or companies. The number of employees employed is unlimited and the income is not more than 7 million UAH. The fourth group is agricultural producers. They sell their agricultural products for more than 75 percent.

The tax rate for each group is explained by Ms. Valentyne as follows. The first group is charged up to 10 percent of their living expenses. The second group is subject to a tax of 20 percent of the minimum cost of living. The third group is subject to a tax of 3 percent of the income from paid VAT and is subject to 5 percent of income if the VAT is not paid. As for the 4th group, it is classified as follows: for suburban, pasture, and hay fields — 0.95% of the normative monetary value; multi-year investment — 057% of Normative monetary value. As for the groundwater fund - 2.43% of the normative monetary value (hectare of suburban land). Meanwhile, land used in closed land conditions = 633% of the normative monetary value (1 hectare of arable land).

Mrs. Valentyna gave a special note regarding this tax rate. A certain rate of fixed tax, applied generally, according to Clause 10.2 of Article 10 of the Tax Code of Ukraine, local councils must establish a single tax.

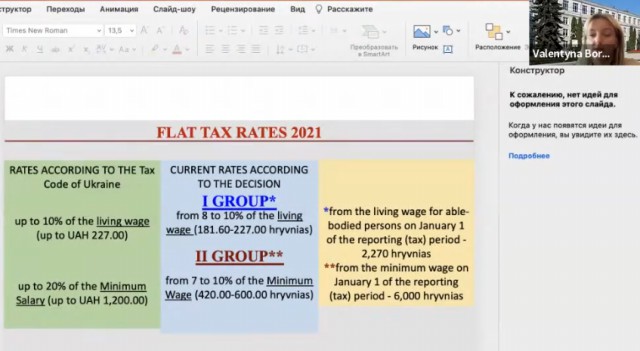

Ms. Valentine explained about the 2021 flat tax in Ukraine. The rate according to the Ukrainian code tax is up to 10% of the living wage (up to UAH 227.00). As for rates of up to 20% of the minimum salary (up to UAH 1200.00). The current rate is according to the decision, group 1 is subject to tax rates from 8 to 10% of the cost of living. Meanwhile, group 2 is subject to a tax rate of 7 to 10% of the minimum wage. The calculation is based on the living wage for able-bodied persons on 1 January reporting period (tax) - 2,270 hryvnias. As for the calculation of the minimum wage in the reporting period January 1 (tax) - 6,000 hryvnia.

Visiting Lecturer from Podilia State University Ukraine 2022 teaching tax management in wartime Part 3

International Webinar

Kembali ke Berita

International Webinar

Minggu, 13 November 2022

Priyadi, S.Kom, M.Kom

0 Dilihat