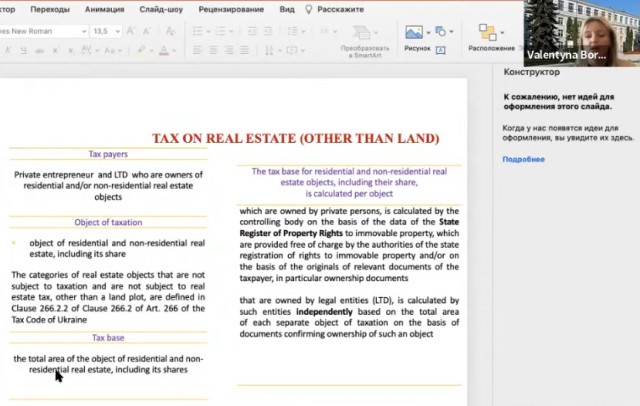

In Ukraine, the tax base for residential real estate and non-residential objects, including their shares, is calculated per object. Tax objects owned by private individuals, are calculated by the supervisory agency based on data from the State Register of Property Rights on immovable property, which are given free of charge by the official for the registration of rights on immovable property and/or based on relevant original documents from the taxpayer, in particular, title documents. As for objects owned by legal entities (LTD), these agencies are calculated independently based on the area of each separate tax object based on documents stating ownership of the object.

How is the implementation of the existing taxation system in Ukraine in conditions? Academics from state universities in Ukraine have given very clear and interesting explanations in an international seminar held by STEKOM University. The title of the Presentation was "Local tax: a system of calculation and payment under martial law in Ukraine". The name of the academic from the State University of Ukraine is Valentyna Borkovska. He has a PhD in Economics. Ms. Valentyna as Associate Professor Educational and Scientific Institute in the department of Accounting, Business and finance, at Podilia State University.

This activity is part of the implementation of STEKOM University's commitment to increase various international activities in order to realize the vision to become an international-class university. Various international activities carried out by STEKOM University continue from year to year. There are sustainable international activities and there are also some unsustainable international activities. All types of international activities are accommodated and regulated by the International department of STEKOM University.

Mrs. Valentyna explained about the taxpayer. Taxpayers are private entrepreneurs and LTD housing owners who own real estate and/or non-residential objects. The explanation then continued about the object of taxation. Residential and non-residential real estate objects belonging to the category of non-taxable real estate objects and non-taxable real estate, other than land plots, are defined in Clause 266.22 of Cause 2662 of Art. 266 of the Tax Code of Ukraine. Furthermore, regarding the target of taxation. Where is the total area of residential objects and non-residential real estate, including distributed objects.

Next, Mrs. Valentyna explained the property tax rates. Property tax is assigned by decision of the relevant council depending on the location (zoning) and the type of real estate object. Total real property tax rate does not exceed 1.5% of the minimum wage established by law on January 1 of the reporting year (tax) for 1 square meter tax base - 90.00 UAH. The amount of the tax increases by UAH 25,000 per year for every residential object whose area exceeds 300 square meters. m (for apartments) and/or 500 sq. m. (for home) - pp 266.7.1-1 Item 266.7 Art. 266 from TCU.

Visiting Lecturer from Podilia State University Ukraine 2022 teaching tax management in wartime Part 4

International Webinar

Kembali ke Berita

International Webinar

Minggu, 13 November 2022

Priyadi, S.Kom, M.Kom

0 Dilihat