How is the implementation of the existing taxation system in Ukraine in a state of war? Academics from state universities in Ukraine have given very clear and interesting explanations in an international seminar held by STEKOM University. The title of the Presentation was "Local tax: a system of calculation and payment under martial law in Ukraine". The name of the academic from the State University of Ukraine is Valentyna Borkovska. He has a PhD in Economics. Ms. Valentyna is an Associate Professor at the Institute of Education and Science in the department of Accounting, Business and Finance, at Podilia State University.

This activity is part of the implementation of STEKOM University's commitment to increase various international activities in order to realize the vision to become an international-class university. Various international activities carried out by STEKOM University continue from year to year. There are international activities that are sustainable and there are also some international activities that are not sustainable. All types of international activities are accommodated and regulated by the International Department of STEKOM University.

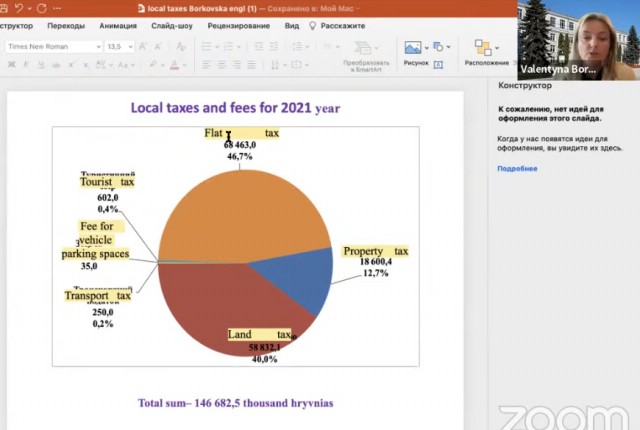

At the start of her presentation, Ms. Valentyna explained that the following local taxes and fees applicable today in Ukraine include: property tax which includes taxes on immovable property other than land, land fees (land and rent taxes), transport taxes; vehicle parking fee; tourist tax; and fixed taxes. Currently, the highest percentage of tax revenue in the country is from a fixed tax of 45.7 percent. Now the tax code sets a flat tax rate of 18% instead of the previous 15/20% tax. These general rates apply to most types of individual income (salary, investment income, etc.). Dividends received from Ukrainian companies are still subject to a 5% tax.

The next highest percentage of tax revenue is the land tax of 40 percent. Now the Tax Code establishes a flat tax rate of 18% instead of the previous 15/20%. These general rates apply to most types of individual income (salary, investment income, etc.). Dividends received from Ukrainian companies are still subject to a 5% tax.

Then followed by property tax revenue of 12.7 percent. The maximum tax rate has been increased from 2% to 3% of the mandatory minimum wage per 1 square meter of property. Owners of residential properties with a total area exceeding 300 sq.m. (for apartments) and 500 sq.m. (for houses) also have to pay UAH 25,000 per year (about USD 1,000) for each of these properties.

Furthermore, Ms. Valentina carried out the legal basis for the formation of regional taxes and levies in Ukraine. Article 143 of the Ukrainian constitution gives city councils the local right to set local taxes and fees. In accordance with Clause 24, Part 1, Art. 26 Law No. 280 "Self-Regional Government", this issue is resolved exclusively at plenary meetings of villages, settlements and city councils. In this case the local council must establish a flat tax and a property tax (in the case of a transport tax and a land tax).

Ms. Valentyna explained that the most important sources for improving general public funds are the land tax, fixed tax and excise tax. The order of local tax revenues and mandatory levies from the highest is fixed tax, land tax and transportation tax. Meanwhile, based on the decision of the specialist commission, property tax is the highest, followed by tourist tax and parking space tax.

Questions regarding the determination of the property tax (within the tax on immovable property, other than land plots) and the determination of fees for parking spaces for vehicles and tourist taxes are decided by local councils within the limits of their powers, the rest is determined by the TCU. An important note by Ms. Valentyna : Local taxes and fees that are not regulated by the Tax Code of Ukraine are prohibited!

Visiting lecturer from Podolia State University of Ukraine 2022 teaching tax management in wartime management Part 1

International Webinar

Back to News

International Webinar

Sunday, November 13, 2022

Priyadi, S.Kom, M.Kom

0 Views